Global Market Update for Inductors, Beads and Cores: March 2025

GLOBAL MARKETS: MAGNETIC COMPONENTS

Paumanok estimates the global magnetic components business at $6.2 billion in market value for FY 2024, of which inductors, EMC components and ferrites account for 45% of worldwide consumption value, and PCB transformers, magnets, sheets and magnetic materials account for the larger 55% of the magnetic component consumption value worldwide.

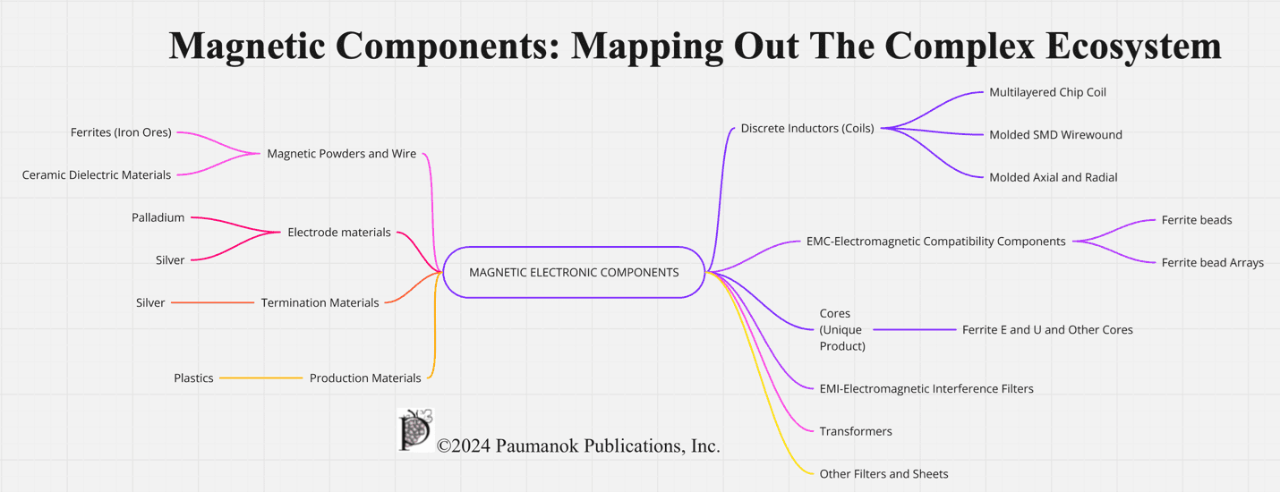

The following chart maps out the complex magnetic components market, including component types and configurations as well as feedstocks, such as metal powder and wire:

Figure 1.0

Structure of the Global Market Components Market in 2025

Source: ©2025 Inductors, Beads and Cores: World Markets, Technologies & Opportunities: 2025-2030 ISBN #1-893211-99-1 (2025)

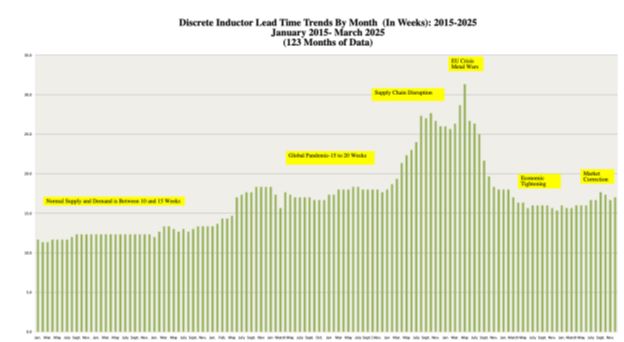

Furthermore, the chart below in Figure 2.0 shows the 123-month collective lead time trend for discrete inductors. In February 2025, discrete inductor demand showed mixed results in lead time from the prior months which is historically indicative of market turmoil, whereby semiconductor chipsets and electric vehicle propulsion are driving up the value of demand for certain magnetic components.

Meanwhile, global attempts to rein in inflation are impacting the portable electronics space, resulting in a substantial slowdown in lead times for ferrite beads and chip coils which rely on these mass-produced end products for volume sales.

Figure 2.0

Inductor Lead Time Trend: 123 Months of Data

Source: ©2025 Inductors, Beads and Cores: World Markets, Technologies & Opportunities: 2025-2030 ISBN #1-893211-99-1 (2025).

DISCRETE INDUCTOR LEAD TIMES

The above chart in Figure 2.0 demonstrates that normal lead times for discrete inductors had been historically between 10 and 15 weeks during normal trading cycles. The pandemic created plant shutdowns and material supply chain disruptions that impacted the entire high-tech ecosystem. Inflation and supply chain disruptions began to impact the global magnetic components markets in the beginning of 2021, causing lead times to rise steadily, reaching 25 to 30 weeks in late 2021 and culminating with a peak during the first phases of the EU war crisis of 2022. Subsequently there was a drastic increase in U.S. interest rates that has had a profound impact on both supply and demand, and, as the chart above shows, the supply chain continues to move back to normal levels of supply and demand.

The inductor big data sets include discrete inductors in these individual types and sub-categories:

Axial and Radial Leaded Micro-Inductors

These magnetic components are ultra-small axial leaded and radial leaded wire-wound inductors, including conical inductors that are consumed in communications backbone electronics, instrumentation equipment and computers. The market experienced a surge in demand during the pandemic due to a solid increase in production of notebook, desktop and server computers. This segment is also growing in the area of satellite communications systems.

Chip Coils

These are ceramic, thick film, surface mount, multilayered or sputtered thin film inductor chips, employing barium strontium titanate. The primary markets are in wireless handsets and automotive electronics. The chip coils are produced in 0201, 0402, 0603, 0805 and 1206 case sizes. Chip coils are largely dependent upon the health of the massive wireless handset and portable computing industries.

Ferrite Beads

These are thick film metal ferrite beads that are produced in 0201, 0402, 0603, 0805 and 1206 case sizes and are consumed for noise abatement primarily in computer markets. The ferrite bead markets also experienced increases in demand during the pandemic due to a rise in consumption of desktop, notebook, server and tablet devices.

COMPONENT LEAD TIMES POINT TOWARD MARKET DIRECTION

Figure. 3.0 below illustrates the lead time trend for discrete inductors by sub-category from January 2015 through the end of February 2025. Some insights into this chart would include the level of disruption experienced by the supply chain due to its reliance on base metals such as iron, nickel, magnesium and zinc. But the 2021 run up in lead times was the result of an unexpected increase in demand for ferrite beads and chip coils from the computer markets. Since then, the inductor markets have returned to their pre-pandemic supply and demand levels.

Figure 3.0

Discrete Inductor Lead Time Trend by Component Sub-Category: 123 Months of Data

Source: ©2025 Inductors, Beads and Cores: World Markets, Technologies & Opportunities: 2025-2030 ISBN #1-893211-99-1 (2025)

CIRCUITS THAT WILL REQUIRE DISCRETE INDUCTORS: 2025-2030

The following are noted end product circuit applications for discrete inductors that drive demand:

Wireless Handset Markets for Discrete Inductors

The inductor markets rely heavily on the handset business to set market direction and return on investment for capacity expansion. The number of viable vendors of quality inductors is limited and many vendors have been attempting to acquire companies in the space to consolidate global production. Wireless handsets consume ferrite beads, arrays and chip coils for impedance matching of circuits and for noise protection in modules, microphones and speaker circuits.

Automotive Markets for Discrete Inductors

Discrete inductors are consumed in automobiles for electric vehicle propulsion and assisted driving circuits. The automotive segment continued to outperform other sectors in the first quarter of 2025, primarily related to real demand for components consumed in converter, inverter, charger and battery management circuits. The automotive markets demand SMD coils, EMC inductive chips and ferrite beads and cores for noise reduction and power circuits in compact sub-assemblies in both the engine compartment and passenger space where electronics are close proximity. This includes components for the stereo, navigation system, XM radio and driver computing. The more demanding circuits for component vendors are for applications in the anti-lock braking system cards, the air bag igniter circuits, tire pressure monitoring and the electrification of the powertrain.

Industrial and Infrastructure Markets for Discrete Inductors

Power supplies and lighting ballasts are important and consistent markets for SMD wirewound; axial and radial leaded micro-inductors. Power supplies are a broad category that include DC motor assemblies; switch mode power supplies and DC/DC converter bricks consumed in industrial automation equipment and advanced robotics. Lighting ballasts are an ecosystem that is separate from the power supply industry because of system architecture and a large, dedicated customer base, although component requirements largely overlap with respect to voltage and performance at higher temperatures.

Computer Markets for Discrete Inductors

Computers require inductors for noise abatement in key circuits. This includes across-the-board applications in desktop, notebook, tablet and server designs with ferrite cores also consumed in key processing applications. Demand from the graphics processing (GPU) markets for noise abatement in compact chip designs remains a significant growth portion of the business in 2025.

Consumer AV Markets for Discrete Inductors

Consumer home theatre electronics, including television sets, are a significant end market for discrete inductors also for noise abatement in compact electronics. Inductors are also found in game consoles and cable set top boxes. This market has shown growth in 2025 for handheld game consoles.

Specialty Markets for Discrete Inductors

Discrete Inductor sales to the specialty markets include sales to commercial aerospace, defense space and medical end markets. This market segment includes mil-spec, medical technology, instruments, lab equipment, space electronics and commercial aircraft, or any circuit requiring a high voltage, high temperature or high frequency magnetic solutions.

TRENDS AND DIRECTIONS IN INDUCTIVE COMPONENTS

Thin Film Ceramic Inductors

The thin film inductor market is just emerging and continuing to expand, and its technology could be extended into extremely small case sizes. The thin film inductor market is based on barium strontium titanate thin film, and the process comes from semiconductor manufacturing which will be critical to all next generation component technology in passives (CRL).

Next Generation 01005 and 008004 Case Size

There is a clear movement toward ultra-small case size ceramic chip inductor technology using photolithography techniques as opposed to the traditional multi-layered stacking technology to achieve the 01005 and new 08004 chip case sizes. The overlap in the 0201 and the 0402 using both thick and thin film solutions is also apparent and the technology in both thick and thin film will continue to develop and grow. All high-volume chip vendors must be focused on new equipment and technology platforms and disciplines required to run thin film, simply because in the mind of the design engineer, the concept of thin film promotes the idea of greater precision and better performance.

Low-Profile Chip Inductors

The lower profile chips are in great demand in modules and handsets so that end products can be thinner in design. This is being accomplished now in inductors through materials selection and technology platform. In thick film, the technology has been amazing and has focused on three-dimensional development of the core spiral. In thin film, the sputtering technique allows for thinner chip designs when compared to thick film solutions, which largely reach their cost effectiveness and return on investment at the 0201 chip size.

Future Markets in THz Frequencies

Future market opportunities for advanced magnetic components are being projected for applications from 300.1 GHz to 3,000 GHz, or into the terahertz range. Potential future applications include terahertz imaging—a potential replacement for X-rays in some medical applications, ultrafast molecular dynamics, terahertz time-domain spectroscopy, terahertz computing/communications, sub-mm remote sensing and geothermal exploration and logging tools.

SUMMARY AND CONCLUSIONS

The inductor market is at the low end of the cycle in 2025 with lead times suggesting a weak market environment for mass produced beads and chip coils but offset positively to support noise abatement in advanced semiconductors (chip coils) and in electric vehicle propulsion (axial, radial, core).

The market for discrete inductors appears to have bottomed out in the first quarter of 2025 with the outlook for ferrites and coils tied largely in movements in the handset and game console business, which constitutes the largest volume consumer of discrete inductors in the world. Continued growth in automotive assisted driving circuits is also expected for all sedans over the next five years as well as continued value growth in electric vehicle converter and inverter boards.

Paumanok Publications, Inc. is the world's largest supplier of market research and consulting services to the passive electronic component industry. For 36 years, Paumanok has supplied research products and services for trade companies and private equity firms that have a financial interest in or are directly involved in the supply chain for capacitors, resistors, inductors and circuit protection components as well as the engineered materials and ores associated with their key functions.

Statements of fact and opinions expressed in posts by contributors are the responsibility of the authors alone and do not imply an opinion of the officers or the representatives of TTI, Inc. or the TTI Family of Specialists.

Follow TTI, Inc. on LinkedIn for more news and market insights.

Statements of fact and opinions expressed in posts by contributors are the responsibility of the authors alone and do not imply an opinion of the officers or the representatives of TTI, Inc. or the TTI Family of Specialists.

Follow TTI, Inc. - Europe on LinkedIn for more news and market insights.

Statements of fact and opinions expressed in posts by contributors are the responsibility of the authors alone and do not imply an opinion of the officers or the representatives of TTI, Inc. or the TTI Family of Specialists.